Already available! The weekly World Economic Digest (Wednesday) on 20.08.2023 presents the most significant economic events and their impact on the world economy. In this issue, we will look at the latest updates in world trade, the development of financial markets, changes in the political situation and their possible impact on international firms and investors.

Eurozone

UK CPI: THE BASELINE INDICATOR RAISES CERTAIN CONCERNS

The growth of consumer prices in the UK in July was 6.8% kg vs 7.9% yoy and 8.7% yoy two months earlier (forecast: 6.8%). Monthly rates: -0.4% mm vs 0.1% mm and 0.7% mm in June-May (forecast: -0.5%). The annual indicator is moving away from the maximum marks that were reached in October last year (11.1% yy)

The biggest contribution to the monthly CPI change was made by the reduction in electricity and gas prices. But prices for transport and hotel services are rising.

At the same time, that the annual pace of the base CPI remained in place: 6.9% yy vs 6.9% yy and 7.1% yy earlier (forecast: 6.8% yy), and monthly – increased: 0.3% mm vs 0.2% mm and 0.9% mm (0.2% mm was expected)

The situation with prices in the UK is still the most problematic among the most developed Western countries. VoE has not yet announced any plans to mitigate its PREP

EUROZONE ECONOMY: SMALL SIGNS OF IMPROVEMENT, GOOD GROWTH IN FRANCE

According to a preliminary estimate by Eurostat, Eurozone GDP growth in 2Q2023 was 0.3% QoQ vs 0.0% QoQ and -0.1% QoQ two quarters earlier. Recall that during the third assessment, the pace of the first quarter was revised up (from -0.1% QoQ to 0.0% QoQ), i.e. there is no recession on the continent. Annual dynamics decreased: 0.6% kg vs 1.1% y.

In the context of countries where the growth rates have become higher, Lithuania (2.8% QoQ vs -2.1% QoQ) turned out to be quite unexpectedly, the rates of steel were higher in Ireland (3.3% QoQ vs -2.8% QoQ) and Slovenia (1.4% QoQ vs 0.7% QoQ). The situation is worse in Italy (-0.3% sqq vs 0.6% sqq) and Austria (-0.4% sqq vs 0.1% sqq)

Leading economies of the region: Germany (0.0% sqq vs -0.1% sqq, recession is over), France (0.5% sqq vs 0.1% sqq).

British inflation has slowed down on tariffs... but it remained high

Consumer prices in the UK fell by 0.4% mom in July, annual inflation slowed to 6.8% YoY, but the Bank of England is unlikely to be happy here, because inflation remains the highest among the largest developed economies, and the slowdown in inflation is again more modest than expected. The slowdown in inflation is based on a planned reduction in gas tariffs (-25.7% mom and 1.4% YoY) and electricity (-8.6% mom and 6.7% yoy), i.e. the effect of rising energy prices has almost gone out of inflation, and inflation has remained high.

Although the impact of food price growth remains partially here (0.2% mom and 14.8% YoY), but commodity prices fell by 1.7% mom and are growing by 6.1% YoY.

But prices for services continue to grow actively by 1% mom, annual growth accelerated to a record 7.4% YoY. As a result, core inflation remained at the June level of 6.9% YoY, which is only slightly higher than the May record of 7.1% YoY. Medicine (8.9% YoY) and restaurants/hotels (9.6% YoY) rose the most cheerfully. In general, core inflation remains extremely high, and the Bank of England’s current rates remain in a deeply negative zone.

The markets, of course, are trying to play a little in favor of the pound and the Central Bank’s tougher policy on the rate, government bond yields are growing again, debt servicing is becoming more expensive, yields are near highs, and it will be increasingly difficult for the Bank of England not to notice this.

#UK #inflation #economy #rates #BOE

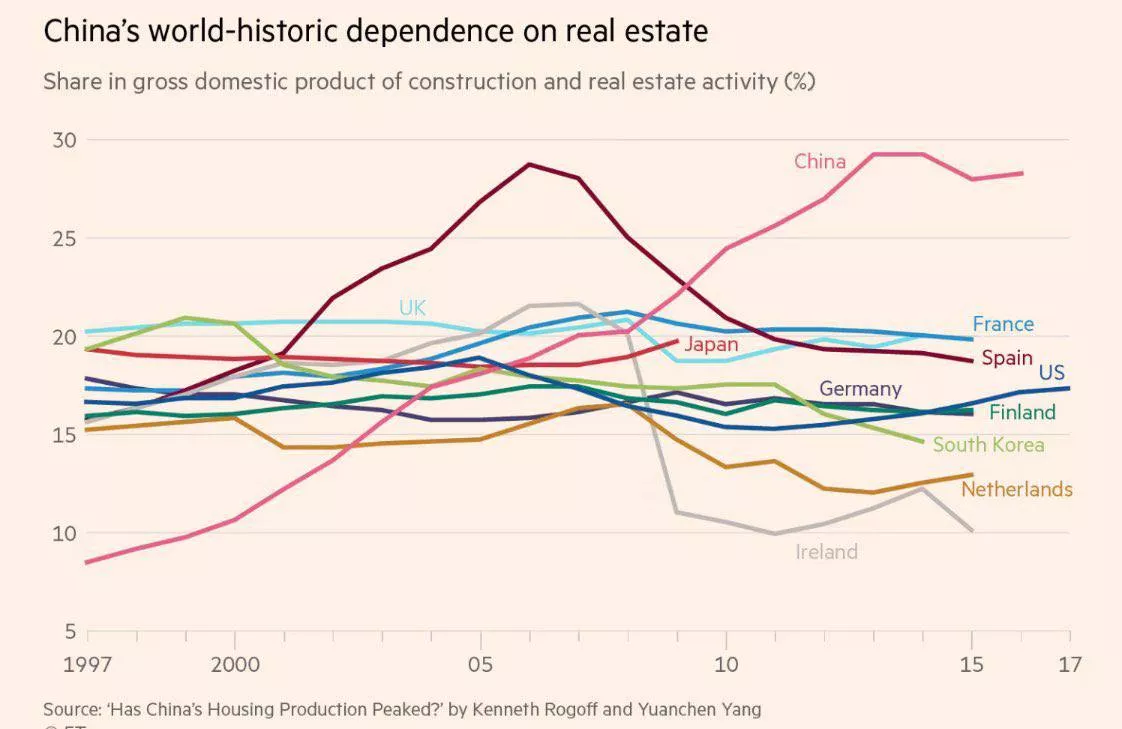

China

The real estate sector accounts for 30% of the Chinese economy.

Currently, there are 50 million vacant apartments in China, which indicates unfavorable prospects in the country’s construction industry. The media are increasingly publishing negative headlines about the economic situation in China and its prospects.

#china #gdp #real estate #economy

Thrifty Chinese …

While everyone is waiting for a decision on the rate of the Bank of Russia, China has published the main economic reports for July:

Industrial production slowed down to 3.7% YoY against 4.4% in June, indicating a deterioration in the dynamics in the manufacturing sector, which is associated with both weakening external demand and weak domestic demand. Adjusted for seasonality, there was simply no production growth in July (0% mom).

Retail sales increased in nominal value by only 2.5% YoY, in real terms, the growth is comparable. Directly in July, retail sales decreased -0.1% mom adjusted for seasonality, a big role was played, of course, by a drop in sales of building materials, but this was offset by an increase in catering costs.

#China #economy #manufacturing #retail #rates

Chinese banks have faced difficulties due to economic fluctuations and growing problems in the real estate market

📌 Chinese banks, which reported earnings next week, are struggling with a number of operational challenges as the economy and real estate market falter.

China Construction Bank Corp., Bank of Communications Co. and China Merchants Bank Co. may face a heavier reserve burden in the second half of 2023 and early 2024 after developer Country Garden Holdings Co. couldn’t pay the dollar bonds on time. Global investors, including BlackRock Inc. and Allianz SE, have also recently invested in bonds.

Banks also faced scrutiny after the shadow bank Zhongrong International Trust Co. missed payments on dozens of products and planned to restructure debt. The liquidity problems highlight how problems in the real estate sector and a weak economy are affecting the financial sector.

According to Bloomberg Intelligence analyst Francis Chan, the impact of local government financial instruments and the deflationary economy exacerbate the pressure.

Chinese Investors rush into municipal bonds, hopes for government support outweigh debt Problems

▪️ China’s promise of a “comprehensive” package to solve local debt problems has caused a stir regarding bonds issued by local government financial institutions (LGFV), as investors feel an implicit state guarantee for these provincial firms.

The yield on LGFV bonds, which account for half of China’s corporate bond market, has fallen to its lowest level this year, even despite the deepening debt crisis in the real estate sector, to which most of them are exposed.

However, investor confidence in LGFV bonds worth about $1.9 trillion returned after the July meeting of the Politburo of China, at which senior politicians announced their intention to develop a comprehensive scheme to eliminate local debt risks.

Chinese Asset Manager Signals Debt Review, Stoking Contagion Fears

A major Chinese asset manager has told its investors that it needs to restructure its debt, raising fears that a chain of defaults could spread to the financial sector and cause a destabilizing shock to the country’s weakened economy.

Zhongzhi Enterprise Group, which raises money from companies and the general public and reportedly manages assets of 1 trillion yuan ($137 billion), spoke about the restructuring at a meeting with investors on Wednesday, as shown by a video viewed by Reuters.

Concerned retail investors are bombarding listed companies with questions about their exposure to Zhongrong, a subsidiary of Zhongzhi, after the trust company’s missed payments raised fears of a wider spread.

India

Goldman: India is becoming popular among foreigners again

According to Goldman Sachs Group Inc., shares of Indian companies with medium capitalization are gaining popularity among foreign investors again after a five-year decline.

“We are seeing a sharp change in the share of foreigners in the ownership of Indian mid—cap companies,” strategists, including Amorita Goel and Sunil Cole, wrote in a note on Wednesday, referring to their analysis of stock ownership data for the second quarter.

They added that the share of foreign investors with average capitalization increased by 175 basis points to 16% of their market capitalization this year, compared with a drop of 250 basis points over the past five years.

The return of the world’s money to smaller and riskier Indian stocks shows their confidence in the Indian stock market, despite concerns about the valuation premium. Small stocks attract foreign buyers, even though they remain more expensive than large ones.

🔺 The S&P BSE MidCap index is up more than 20% this year, surpassing the 7.4% gain in India’s benchmark stock index. According to data compiled by Bloomberg, it trades 24 times on a profit-based valuation, versus 19 times on the Sensex index.

According to data compiled by Bloomberg, the Indian stock market has received about $15.5 billion in net foreign exchange inflows this year, which is almost $1.5 billion less than last year’s record outflow. This support helped Sensex to rise by 14% compared to the March low amid minor changes in the indicator of emerging market stocks due to the sell-off of risky assets in China.

* According to Goldman strategists, international investors preferred Indian stocks focused on the domestic market more than local investors, while their share increased most in the consumer and cyclical sectors.

USA

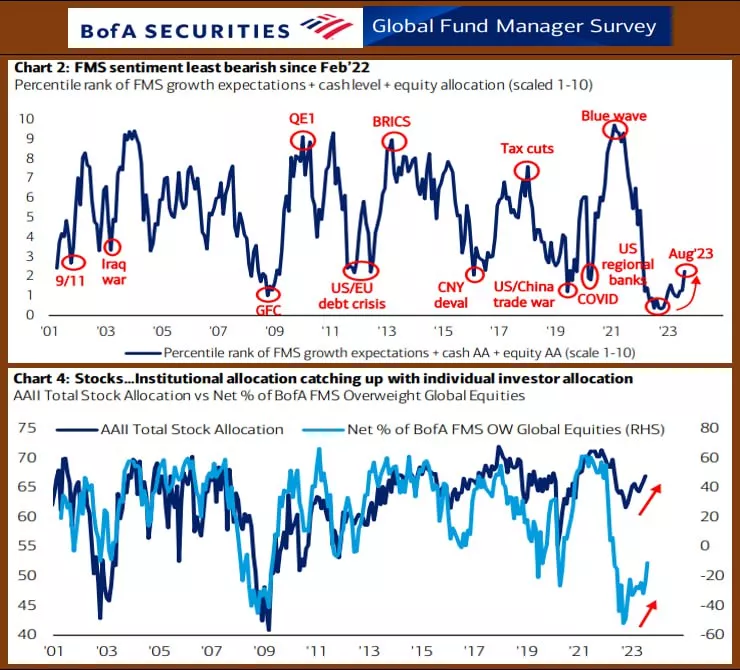

BofA GLOBAL FUND MANAGERS SURVEY: OPTIMISM HAS GROWN SIGNIFICANTLY, ESPECIALLY IN STOCKS

The result of the August survey of managers (Global FMS):

• Least bearish FMS since February 2022

• Global economic growth expectations: 4/10 say a recession is “unlikely” (it was 1/10 in November 2022)

• Forecasts for the start of Fed rate cuts are now the highest since November 2008.

• Three quarters of respondents expect a soft landing of the American economy

• The CASH level has significantly decreased: from 5.3% to 4.8%, this is a 21-month low

• The lowest Underweight in stocks since April 2022,

• The largest Overweight in Tech stocks since December 2021

USA: SOME RECOVERY IN INDUSTRY, AND MORE OBVIOUS - IN CONSUMER DEMAND

Industrial production index in July: 1.0% mm vs -0.8% mm and -0.5% mm. Annual dynamics: -0.23% yy vs -0.78% yy . We were waiting for 0.3% mm and -0.1% yy.

Extraction: 2.0% vs 2.8% yy in June, processing: -0.7% yy vs -0.3% yy, utilities: -0.9% yy vs -6.2% yy . For some subcategories in processing , the dynamics are as follows – consumer goods: 0.2% yy vs -0.7% yy earlier, equipment: – 0.2% yy in these two months, building materials: -2.7% yy vs -1.1% yy

Retail sales (non-inflation adjusted) in the States showed an improvement in dynamics in July: 0.7% mm vs 0.3% mm, annual rates: 3.17% yy vs 1.6% yy. The figures came out noticeably better than expected in 0.4% mm and 1.5% yy. The base indicator was also higher: 1.0% mm vs 0.4% mm with a forecast of 0.1% mm.

By breakdown, the growth is shown by purchases in online stores (1.9% yy), sports and hobbies (1.5% yy), catering (1.4% yy), and clothing (1% yy), while cars (-0.3% yy), furniture stores (-1.8% yy), electronics decreased (-1.3% yy).

LEADING INDICATORS OF LEI: THE FALL CONTINUES

The US Leading Indicators Index (LEI) calculated by the Conference Board decreased from June 106.2 to 105.8 points in July, this is -0.4% mm and -9.1% yy vs -0.7% mm and -9.4% yy a month earlier. This is the sixteenth consecutive month of falling LEI.

The Conference Board notes that “… the prospects remain very uncertain. Weak new orders, high interest rates, a deterioration in consumers’ perception of the prospects for business conditions and a reduction in working hours in the manufacturing industry contributed to the decline of the leading indicator, which still indicates that economic activity is likely to slow down and turn into a moderate recession in the coming months. Now the Conference Board predicts a short and shallow recession in the period from the 4th quarter of 2023 to the 1st quarter of 2024…”

FED: THE RHETORIC REMAINS QUITE TOUGH, DO NOT COUNT ON A RATE CUT THIS YEAR

The Federal Reserve’s balance sheet has shrunk by $67 billion over the past week. vs +$1 billion a week earlier. Now it is $8.197 trillion. From the highs ($9.015 trillion), the balance decreased by -$818 billion

The rhetoric of the Fed representatives:

Williams, Harker:

• the rate may be reduced, but not earlier than 2024

Bowman:

• I do not rule out a further increase in the rate

Harker:

• we have to keep the bid high for a long time

Given:

• it is very premature to talk about a rate cut

Kashkari:

• * uncertainty that enough work has been done to reduce inflation

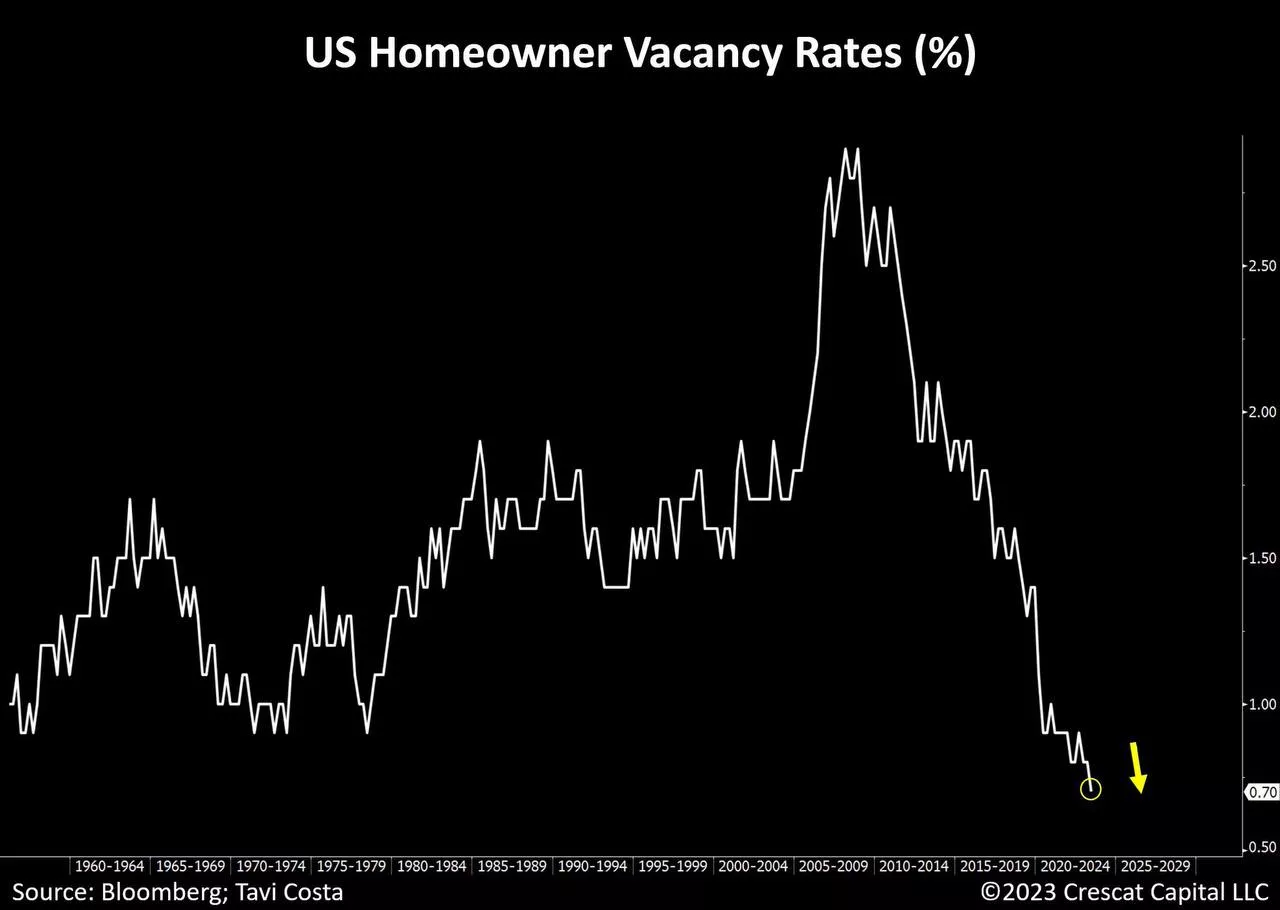

This chart has changed my understanding of the real estate market in the United States, and I think it will cause you a similar reflection.

The share of unoccupied space in the American real estate market has reached its lowest values in the last 60 years. Consequently, there is a housing shortage, in contrast to the surplus before the mortgage crisis of 2008.

Experts in the field of real estate in the USA note that the deficit is associated with the active purchase of space by funds and other institutional investors. If this is the case, then it distorts the real demand, since eventually people should live in these premises. The funds, in fact, act as intermediaries, and the question of whether they will be able to sell the acquired areas remains open. Only then will the real demand become clear.

Regardless of the real reasons for the high demand in the American real estate market, today the construction sector in the United States remains stable, supporting the demand for materials and labor resources, which, in turn, contributes to inflationary processes.

#usa #real estate #economy #housing

The graph of expectations regarding the prospects of the American economy of CEOs, who expected the worst last year, looks interesting.

When earlier CEO expectations were at lows, the S&P500 index also set a multi-year low.

In my opinion, the current situation in the US economy and stock market can be compared with the 70-80 years of the last century. This makes it pointless to compare the cycles of events in the current century, since the influence of inflationary processes can violate any established patterns.

However, the revealed pattern has its own value: only in the case of a decrease in inflation, we can expect a strengthening of the US economy and stock market. So far, the data for July signal stable inflationary processes.

#forecasts #estimates #usa #ceo #economics #analytics #sp500

USA: consumer consumes

Last week, data on manufacturing and retail in the United States were released, retail sales increased by 0.7% mom, which is quite good, considering that quite volatile car sales even declined in July. In real terms, sales have also grown, although fluctuations have been occurring here for a long time without obvious dynamics, just after a sharp increase in covid, sales have stabilized at historically high levels. Excluding cars, gasoline and food, sales increased by 1.1% mom and 5.9% YoY. In general, the American consumer is quite indifferent to the Fed’s attempts to slow down demand.

Production in the United States in July increased by 1% mom, but the data for the past months revised down, because the annual dynamics remained negative -0.2% yoy. In the manufacturing industry, the situation is worse +0.5% mom, but -0.6% YoY. At the same time, capacity utilization at sufficiently high levels and significantly increase production will not work, which in itself is an inflationary factor.

The Fed’s minutes are not aggressive in general, but the markets have tightened, because “most central bank officials still see significant risks of rising inflation, which may require further tightening of monetary policy.” Against this background, the pressure on risky assets has increased, bonds have gone under a new wave of sales, which is reinforced by large budget deficits (which keep the economy overheated). In reality, this only increases the likelihood of a scenario where problems will first come to the financial sector, which will be increasingly affected by the rate increase that has already occurred, and only then will they reach an economy that is under strong budget support… while.

Government bonds have gone to new highs, mortgage rates in the US have reached records since the early 2000s, it should be interesting in the fall and winter.

#USA #economy #retail #manufacturing #rates

⚡️ S&P: on all shoulders... records

The July report on margin positions on the US stock market set new records – the volume of margin positions increased by $29 billion in a month to $710 billion – the maximum since last spring. Although this is still below the records of 2021, when there was more than $900 billion, but the situation is objectively different, because there was only $148 billion of free cache on margin accounts.

As a result, the ratio of the volume of margin debt to free balances on margin accounts flew up to 4.8, i.e. we see a record leverage on the American market by the end of July, with a slowdown in market growth. A large leverage is always the pain of margin calls and corrections during a market reversal.

In June, it also turned out that in addition to the growth of margin positions, foreigners also aggressively bought up American stocks. For the first time in history, inflows into stocks exceeded $120 billion in one month. On the AI-HYIP, both foreigners and Americans were tightly packed into the market… the latter are in debt with a far from low cost margin, given the Fed’s rate hike. To this it is worth adding another background of cashbacks, which will shrink as the profits of companies shrink against the background of rather expensive borrowings.

#USA #SP #stocks

Powell and Yellen are miracles of balancing act...

The Fed’s assets decreased by an impressive $62.5 billion this week, of which the portfolio of government bonds decreased by $42.4 billion, but there was no less money in the system. Because the US Treasury this week reduced its “cache” balance on the Fed’s accounts by $47.4 billion to $384.8 billion at once – in fact, Powell withdrew it synchronously, Yellen added not for the first time, which indicates a fairly high level of coordination. At the end of September, the US Treasury wants to have $650 billion of “cash” in the account.

At the same time, Yellen’s office continued to increase debt, and not only spent its cash reserve – since the beginning of the month, market debt has increased by $ 142 billion and everything is still following the trajectory of further growth of the budget deficit in August, although it has not been the whole month yet – we’ll see.

As a result, despite a rather sharp reduction in the Fed’s balance sheet, the banks did not have much less money. But if the Finance Ministry implements its plan, it will need to withdraw more than $250 billion from the system by the end of the quarter, especially in September, when there is usually a budget surplus. There are no fewer dollars in the system yet, but the supply of public debt is growing (both due to loans from the Ministry of Finance and due to a reduction in the Fed’s portfolio), which continues to put pressure on yields – the public debt curve is growing. Yellen has to give a premium on bills relative to the futures curve.

At the same time, the balance sheets of money market funds continue to swell, which have grown to a record $5.57 trillion, i.e. by $0.75 trillion since the beginning of problems in the banking sector. In autumn and winter, the momentum of monetary tightening will increase, and the fiscal momentum (given the growing cost of debt servicing) will have to be reduced.

#USA #inflation #economy #Fed #debt #rates #dollar

Commodity

Comparison of forecasts of the market of “critical” minerals (important for energy transfer) August 2023 from the International Energy Forum (IEF)

The New World Gas Order: Prospects for 2030 (July 2023) from The Oxford Institute for Energy Studies

Crypto

Results of the day, August 14

🇷🇺 The euro exchange rate on the Moscow Exchange exceeded 111 rubles for the first time since March last year, the dollar is more expensive than 101 rubles.

Today Telegram turns 10 years old — Pavel Durov said that during this time more than 800 million people have registered in the messenger, only thanks to word of mouth.

🕵️♂️ Scammers deceived a Muscovite for more than 23 million rubles in BTC — the guy met with “traders” on Instagram and they promised him to increase his capital through trading on the stock exchange.

👀 Someone accidentally leaked $2 million — the user sent 2 million aUSD to Binance to the USDT address, now he is asking for help.

💰 The payment giant PayPal has announced the launch of a crypto hub “for selected users”.

🇨🇦 The Coinbase crypto exchange is being launched in Canada.

🏡 Huobi founder Li Lin bought a house in Hong Kong for $128,000,000 — this is one of the most expensive mansions in the country.

Elon Musk’s company has received a license to provide payment services in the U.S. state of Georgia.

Justin Sun stated that he is a supporter of the first cryptocurrency and is now spending more than 100,000 BTC.

A bitcoin whale with 1005 BTC ($29.8 million) on its account woke up after 13 years of hibernation.

Results of the day, August 15

The publisher of the GTA series of games, Take-Two company, launches the first crypto game called Sugartown on the Ethereum blockchain.

👁 Big brother is watching you through the keyboard.

A Chinese resident was sentenced to 9 months in prison for buying 13,000 USDT — he will also be required to pay a fine of 5,000 yuan ($690).

📊 BTC volatility has updated the absolute minimum. The indicator stopped at 15.52%. The previous low of 18.91% was recorded on January 12, 2018.

The Central Bank of the Russian Federation and a group of banks are beginning to test the digital ruble (CBDC).

👀 With Gemini, 10,798 BTC and 39,540 ETH were withdrawn in two transactions in a short period of time — a total of $390 million.

Binance has filed a petition against the SEC in court — the exchange wants the regulator to be banned from interrogating witnesses on issues beyond the scope of the case.

🇪🇺 The first spot Bitcoin ETF with the ticker BCOIN has been launched in the European Union on the Euronext Amsterdam exchange.

Results of the day, August 16

Uzbekistan has allowed two private banks to issue cryptocurrency cards.

💸 Yuri Dud advertises Binance.

🔪 An American crypto investor was found dismembered in Bulgaria — a familiar bartender was involved in the murder.

52 years ago, Richard Nixon abolished the gold standard.

The head of the SEC has shown interest in regulating the artificial intelligence market.

Elon Musk said that Mark Zuckerberg refused to fight with him in the Roman Colosseum. Now he hints that the idea of a duel is a joke.

🪙 Donald Trump owns approximately $5 million in Ethereum, new financial reports show, confirming the source of income — the sale of NFT and royalties.

The author of the bestseller “Rich Dad, Poor Dad” and entrepreneur Robert Kiyosaki predicted a rise in the price of BTC to $ 1 million in the event of a collapse of the global economy.

On August 16, Binance will stop the operation of the platform for exchanging fiat for the Binance Connect cryptocurrency (Bifinity).

💸 Coinbase has received approval to trade cryptocurrency futures in the United States.

Results of the day, August 17

Salvadoran cryptans teach 12-year-olds how to send BTC.

🧬 The Shiba Inu meme project has launched its own L2 blockchain on Ethereum called Shibarium – the network has already broken down, and $2.6 million of user funds are now temporarily blocked.

Polygon Labs has entered into partnership agreements with a major Korean telecom operator SK Telecom.

China will allocate more than $34 billion for the creation and development of a Metaverse in Sichuan Province.

Hackers from the DPRK in 2023 stole over $180 million in cryptocurrencies — in total, since 2015, North Korea has stolen virtual assets worth more than $1.5 billion.

Opinion: if the SEC gives the green light to Bitcoin ETF, the first cryptocurrency will be able to overcome the $150,000 mark and approach $180,000.

🪙 Tether will stop issuing USD₮ on Omni, Kusama and Bitcoin Cash SLP from August 17.

Results of the day, August 18

🐹 Against the background of news about the possible bankruptcy of Evergrande and the sale of Cue Balls by SpaceX, the crypto market has fallen.

🪙 Tonight, one trader was liquidated by $55.92 million on Binance — he had 38,896 ETH in the long.

Roskomnadzor restored access to the OKX exchange for users from Russia.

The British payment provider Checkout terminated the contract with Binance due to problems with compliance with regulatory requirements and AML.

🪙 Dogecoin-whales are actively accumulating coins.

Tether Technical Director Paolo Arduino announced 3 new mass products by the end of the year.

⛔️ Hackers hacked the vending protocol Exactly Protocol in the second-level network of Optimism and brought out more than 7160 TK (~$12 million).

The court rejected Coinbase’s motion to lift sanctions against Tornado Cash.

🪙 15 years ago, on August 18, 2008, the anonymous creator of Bitcoin Satoshi Nakamoto registered the domain bitcoin․org.

CALENDAR OF EVENTS FOR THE WEEK FROM AUGUST 21 TO 25

Monday 21.08

• 🇨🇳 China, Central Bank meeting (est. 3.40%, -15 bp)

Tuesday 22.08

• 🇺🇸 USA, second home sales, July (est. 4.15M)

Wednesday 23.08

• 🇦🇺,🇯🇵,🇪🇺,🇩🇪,🇫🇷,🇬🇧,🇺🇸, Flash PMI (August)

• 🇺🇸 USA, new construction, July (est. 701K)

* • USA, building permits,July (est. 1.442K)

* 🇷🇺 Russia, weekly inflation MMI Forecast: 0.05%

• 🇷🇺 Russia, industrial production, July

Thursday 24.08

• 🇹🇷 Turkey, Central Bank meeting

• 🇺🇸 * USA, Initial Jobless Claims (asp. 244K)

• 🇺🇸 USA, Jackson Hole Symposium 24-26.08

• 🇺🇸 USA, the sale of goods lasts. usage (est. -4.0% mm)

Friday 25.08

• 🇩🇪 Germany, GDP, 2Q23 (est. 0.0% mm, -0.2% yy)

News faster in telegram

https://t.me/stockesg – group

https://t.me/ESG_Stock_Market – channel

@ESG_Stock_Market