Morgan Stanley, Sarah Wolfe on behalf of (chief economist) Ellen Zentner:

When Little Pent-Up Demand Is Left

An extraordinary rise in spending on services, combined with a modest recovery in the consumption of goods, led to a decrease in the personal savings rate by a ten-year minimum. Now the recovery of real spending on services is almost complete, which means that the growth of spending on services should slow down, while spending on goods continues to return to its pre-Covid share of income and PCE. Since spending on services accounts for 65% of the share of consumer wallets, the slowdown in growth contributes to lower inflation in the service sector. We expect that a further return (to past levels) of goods consumption, combined with weak growth in the services sector, will allow the Fed to approach the 2% inflation target without causing a recession.

Let’s rewind 2.5 years ago. It’s January 2021, and households are gradually coming out of the hibernation caused by Covid, but the widespread spread of the vaccine is still a few months away. Consumers allocate 5% more funds from their wallet for goods than before Covid, which contributes to record consumption of consumer electronics, household and repair goods, sporting goods and recreational vehicles. Also 2.5 years ago, we made a highly competitive forecast that the spread of the vaccine in the spring of 2021 would lead to a sharp increase in costs for services and payback of goods.

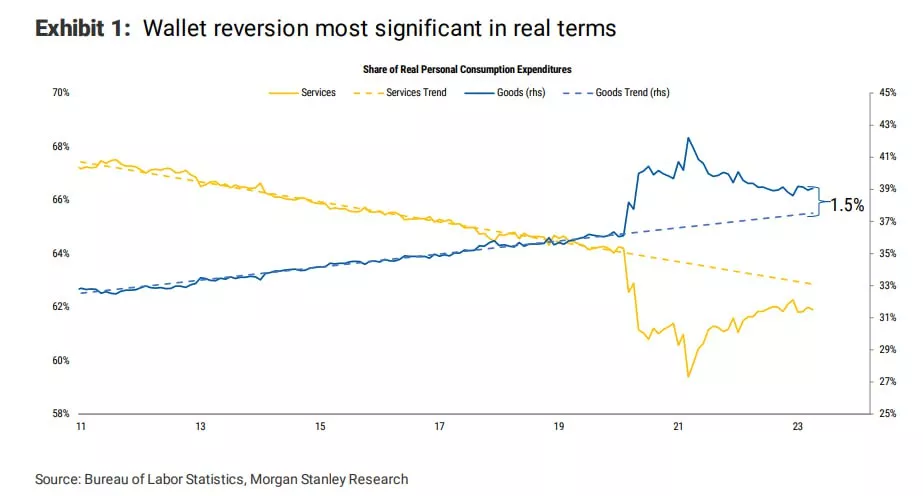

This return has occurred, but paired with greater-than-expected demand, thanks to unprecedented fiscal stimulus, excess savings and a substantial supply shortfall. Thus, we observed not only a shift from goods to services, but also an increase in total spending. The result was a 13 percent increase in goods inflation for almost three years, an acceleration in services inflation and a return to pre-Covid spending habits, which are much larger in real rather than nominal terms. (Figure 1). The biggest gain from Covid was received by stay-at-home products….

..and we have seen the most sustained recovery in discretionary services, including catering, accommodation, public transport and recreational services.

The increase in interest rates led to a decrease in spending on durable goods, which contributed to a slowdown in core goods (2.1% YoY as of April 2023 compared to 9.7% yoy a year ago and we expect that further deflationary pressure will reduce it to -0.2% YoY by December 2023 and to -1.3% YoY by December 2024.). As the supply of labor increases and deferred demand decreases, the pressure on inflation in the service sector begins to weaken. Inflation of basic goods is projected to decline further, and core-core services (core services excluding housing and medical prices) inflation has begun to slow down and as of April 2023 increased by 6.6% YoY, down from a peak of 7.4% in February 2023. The greatest impact on core-core services should occur in the second half of 2023 (5.4% YoY by December 2023 and 4.2% YoY by December 2024).

The growing savings rate leads to a reduction in the overall “pie” of spending, and households have a reduced need and desire to spend on goods and services. This makes it easier for the Fed to achieve the 2% inflation target without causing a recession. There is a potential to reduce the consumption of goods due to reduced needs and rising prices, as well as opportunities to slow down the consumption of services without it becoming negative. Real consumption of services, which increased significantly in 2021 (6.3% YoY) and 2022 (4.5% YoY), is expected to return to pre-Covid levels in the future. @ESG_Stock_Market