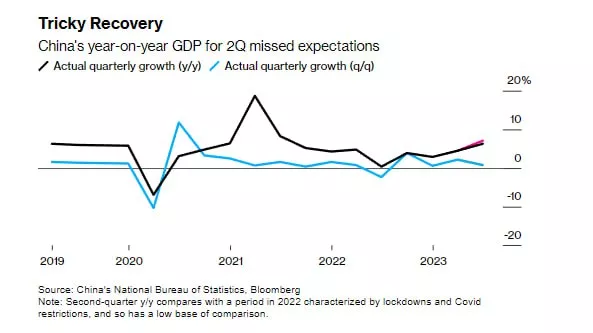

China’s Top Leadership is Likely to Disappoint with Incentives

Economists say that this week China’s top leadership probably will not be able to provide a large-scale stimulus for the weakening economy, which disappoints financial markets waiting for decisive action to counter the downturn.

The July meeting of the Politburo of the Communist Party, the highest decision-making body headed by President Xi Jinping, usually concerns economic policy. Senior officials do not usually announce specific measures at these meetings, but the political tone and language of the statement will provide important clues about how Beijing will respond in the coming months.

Economists say that the meeting is likely to give more signals in favor of growth, which may lead to an increase in budget spending, a moderate reduction in interest rates and additional easing of real estate policy. According to them, the support of the private sector may become the main task after Beijing’s recent promises.

The meeting is likely to “refrain from giving a ‘strong medicine’ to the economy,” said Bruce Pang, chief economist and head of Greater China research at Jones Lang LaSalle Inc. “There won’t be the overly aggressive stimulus policy that the markets were expecting.”

🔸Investors are already lowering expectations and preparing for a prolonged gloom in the stock market. The benchmark index showed its worst week in the last four last week, despite several recent promises by Beijing to increase consumption and support business.

The authorities are resisting the incentives they applied during past recessions to avoid over-stimulating the real estate market and increasing the debt of local governments, which already have a large share of borrowed funds. Beijing is focused on improving the quality of growth, not the pace, and has set a relatively conservative target of about 5% for this year, which it is still largely aiming for.

#china #incentives @ESG_Stock_Market